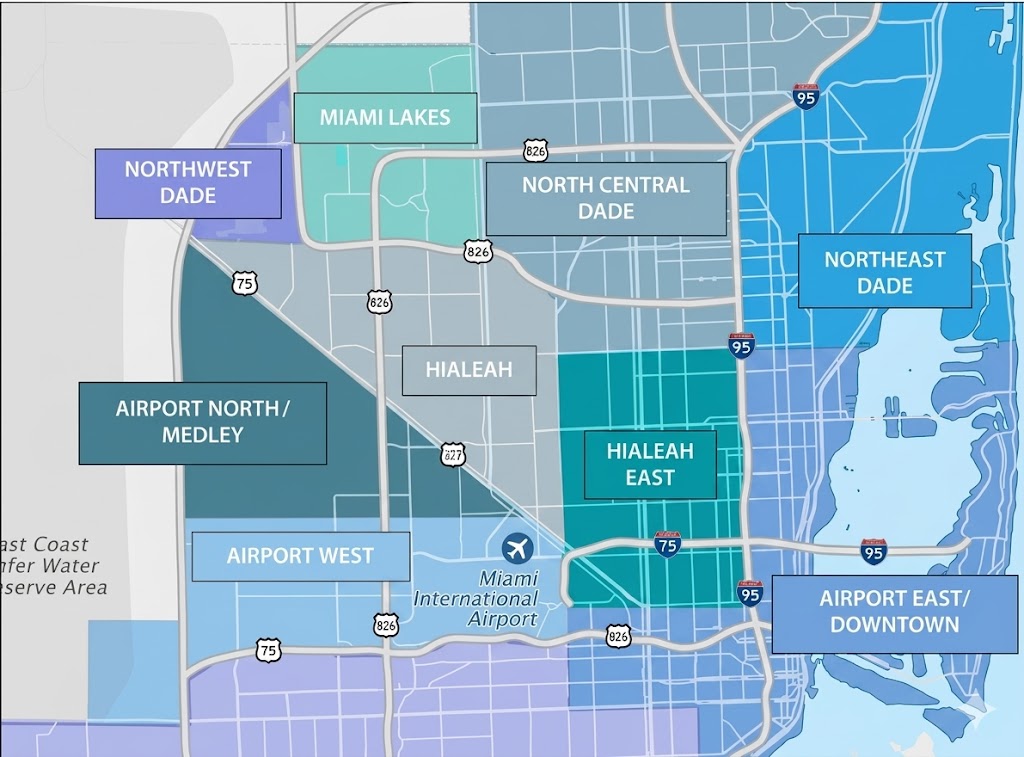

Miami’s industrial market has seen a slowdown in net absorption, dropping to 1.9 million SF over the past year, below the prepandemic average of 3.1 million SF. This decline is attributed to the departure of transportation tenants, leading to a rise in vacancies to 3.4%. Despite this, Miami’s market conditions remain tight, with vacancies well below the national average. Landlords have taken advantage of this by increasing rents by 6.4% annually. Despite the recent moderation in rent growth, Miami continues to be a crucial logistics hub, attracting demand from importers and exporters due to its international connections. The Everglades’ barrier limits new development, ensuring vacancies remain low. Sales volume has returned to pre-pandemic levels, indicating ongoing investor confidence.