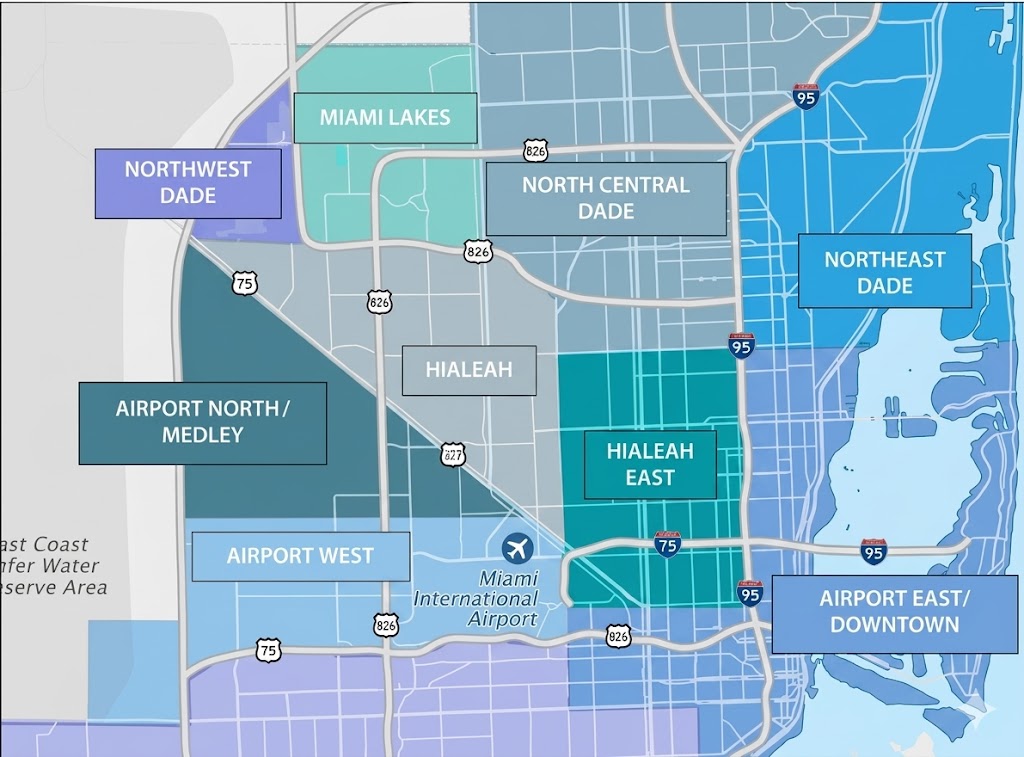

Miami’s industrial market has slowed, with net absorption dropping to -2.0 million SF, well below the pre-pandemic average. Large tenants like UFP Industries and USPS have vacated spaces, pushing the vacancy rate up to 5.7% in Q1 2025, though still below the U.S. average of 6.9%. Despite 5.1 million SF under construction, modern logistics space remains scarce, with properties built from 2015-2023 97% leased locally. Rent growth has slowed to 3.4% in the past year, down from 16% in 2022, and is expected to moderate further. Miami’s strategic position as a logistics hub, with top ports and airports, drives demand. Limited development due to geographic constraints keeps vacancy rates low, with rent growth likely to reaccelerate in 2026. Despite rising interest rates, sales activity picked up late last year, with major acquisitions by prominent buyers.