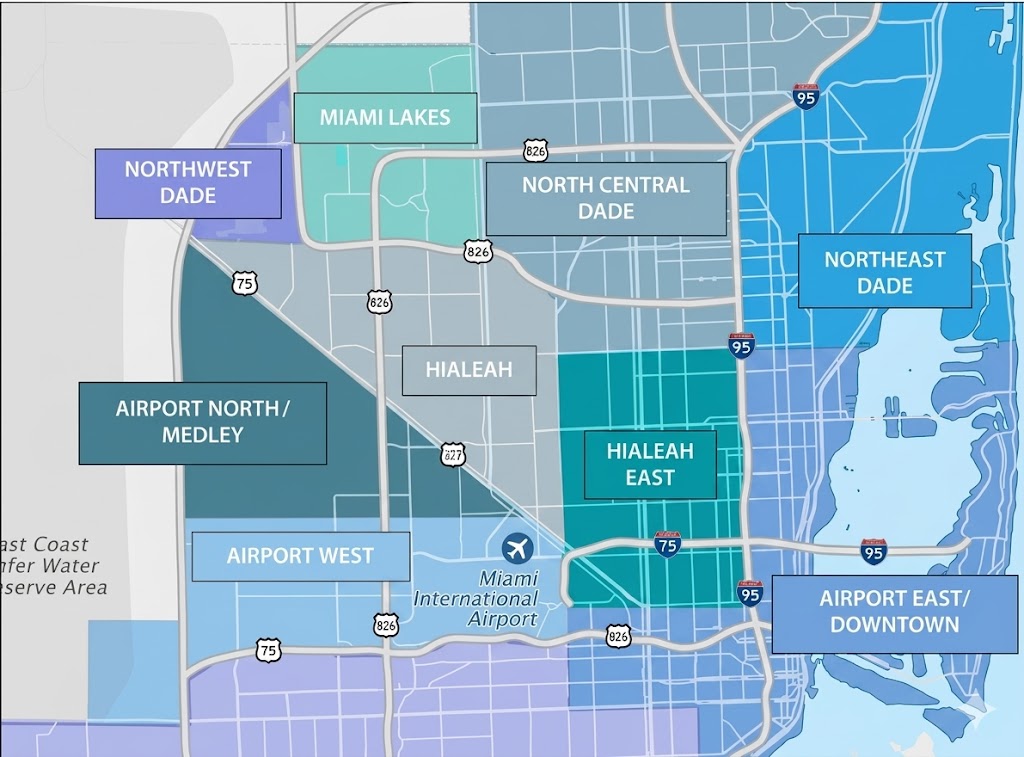

Over the past 12 months, Miami’s industrial net absorption fell to 2.0 million SF, well below the pre-pandemic average of 3.1 million SF, as key tenants vacated large spaces, pushing the vacancy rate from 2.0% in 2022 to 4.8% by Q3 2024. Despite slowdown, vacancy rates remain lower than U.S. average, with limited available space. Miami’s logistics properties, around 85% leased, have allowed landlords to raise rents by 2.9%, though rent growth has cooled from the 17% peak in 2022. Geographic constraints, like Everglades, kept vacancy rates low, supporting future rent growth by 2025-2026. Miami remains a critical logistics hub, with MIA leading in international shipping and the Port of Miami ranking 11th nationally in container traffic. Property sales, which slowed in 2023 due to rising interest rates, saw major acquisitions in late 2023 by prominent buyers.